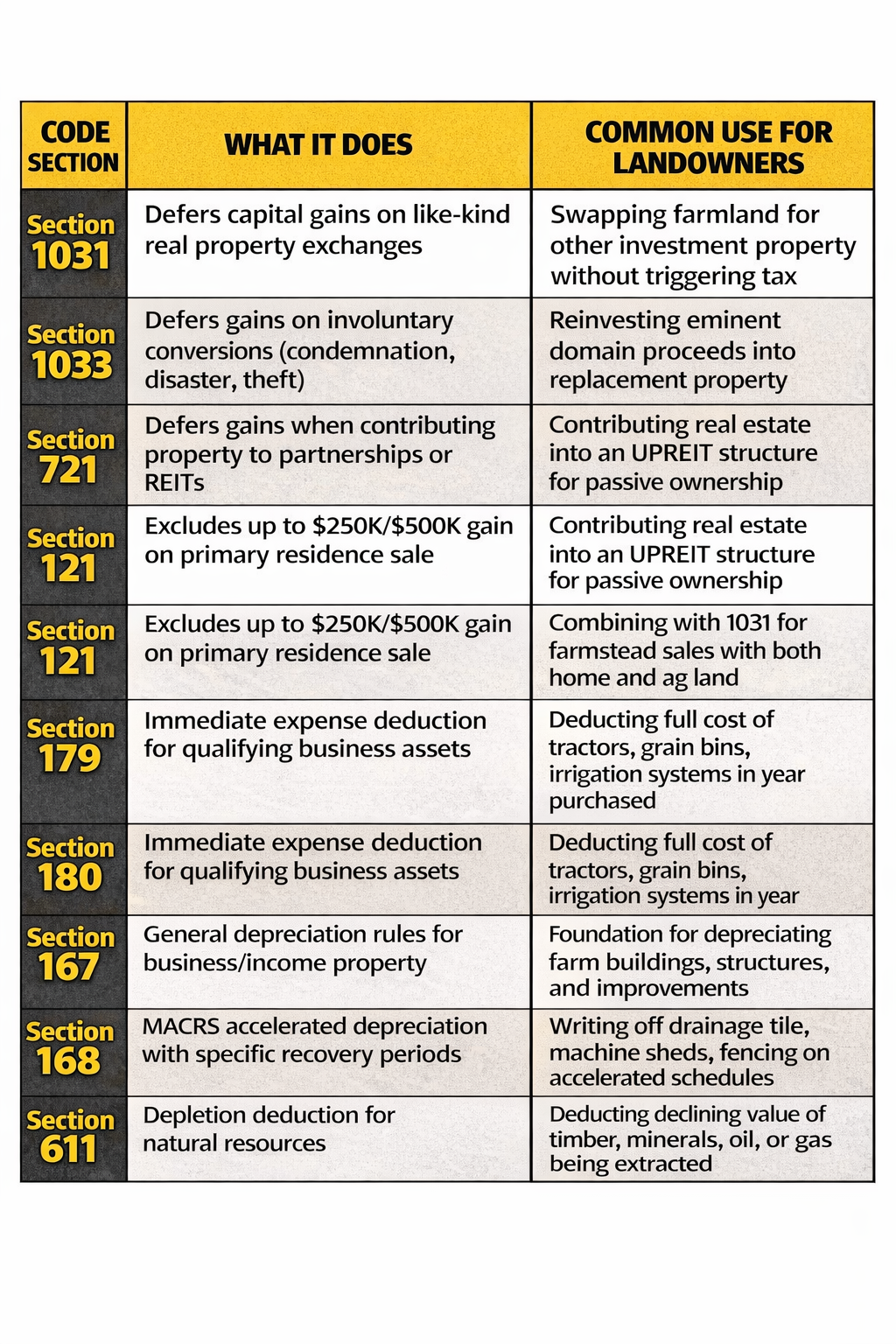

The Tax Code Sections Every Landowner Should Know About

The IRS isn't always the bad guy. These code sections were built to help people like you, if you know they exist.

Here's something that surprises a lot of landowners: the tax code actually has quite a few provisions that were specifically designed to benefit people who own land, farm it, invest in it, or manage natural resources on it.

The problem is that most people never hear about them until it's too late. They sell a property and get hit with a tax bill they didn't expect. Or they spend years paying more than they need to cause nobody walked them through the options that were available the whole time.

This post is meant to change that. We're going to walk through the major IRS code sections that matter most to landowners, farmers, and real estate investors, especially with those in the agricultural space. This isn't a substitute for sitting down with a qualified CPA or tax attorney, but it will give you a foundation so that when you do have that conversation, you know the right questions to ask.

Let's get into it.

Section 1031: Like-Kind Exchanges

This is the one most landowners have at least heard of, and for good reason. It's one of the most powerful tax deferral tools in the entire code.

What it does: Section 1031 allows you to defer capital gains taxes when you sell real property held for business or investment use, as long as you reinvest the proceeds into another qualifying property of equal or greater value. The IRS calls this a "like-kind" exchange, and the definition is broader than most people realize. You don't have to swap farmland for farmland. You could exchange a quarter section of cropland for a multifamily apartment building, an industrial warehouse, or even a fractional interest in institutional grade commercial real estate through vehicles like Delaware Statutory Trusts (DSTs).

Why it matters for landowners: If you've held farmland for decades and the value has appreciated significantly, selling outright can trigger a massive capital gains bill. A 1031 exchange lets you move that equity into a new investment without the IRS taking a cut at the time of sale. And if you continue exchanging throughout your lifetime, your heirs may eventually receive a stepped up basis, potentially eliminating those deferred taxes altogether.

Key details to know: Once your property sells (Day 0), you have 45 days to identify potential replacement properties, and you must close on the replacement by Day 180. An exchange accommodator must hold the funds during the process because you cannot have direct access to the sale proceeds. The same taxpayer must be on the title for both the sold and purchased properties.

For many landowners, this is the section that changes the entire conversation about whether and how to sell.

Section 1033: Involuntary Conversions

This is the section most people have never heard of, until they suddenly need it.

What it does: Section 1033 provides tax deferral when property is involuntarily converted, meaning it's lost or taken from you through events beyond your control. This includes condemnation through eminent domain, theft, destruction from natural disaster, or casualty loss.

Why it matters for landowners: If a government entity takes your farmland for a highway project, pipeline easement, or public infrastructure through eminent domain, you don't necessarily have to pay capital gains taxes on the proceeds. As long as you reinvest in qualifying replacement property within the required timeframe (typically two years, though extensions may apply in certain condemnation situations), you can defer the gain.

A real world scenario: Imagine you own farmland that's been in the family for generations with a very low basis. A state DOT condemns 80 acres for a road project and pays you fair market value. Without Section 1033, you'd owe capital gains on the difference between your basis and the condemnation proceeds. With 1033, you can reinvest those funds into similar property and defer the tax entirely.

This section doesn't get discussed enough, but for landowners in areas where infrastructure projects, pipelines, or government acquisitions are happening, it's essential knowledge.

Section 721: Contributions to Partnerships or REITs

This one is more specialized, but it's becoming increasingly relevant as landowners look for ways to transition from active ownership to passive investment.

What it does: Section 721 allows you to contribute real property to a partnership or a Real Estate Investment Trust (REIT) in exchange for partnership interest or operating partnership (OP) units, without triggering a taxable event at the time of the contribution.

Why it matters for landowners: This is the code section behind what's known as a 721 UPREIT (Umbrella Partnership Real Estate Investment Trust) exchange. Here's how it often works in practice: a landowner first completes a 1031 exchange into a DST, holds that DST investment for the required period to satisfy the "held for investment" requirement, then rolls it into a REIT under Section 721. The result is that the landowner moves from directly owning and managing real estate to holding units in a large, professionally managed real estate portfolio, all while continuing to defer taxes.

This path can also provide a clearer route to liquidity over time, since REIT OP units may eventually be redeemed for REIT shares or rash, depending on the striction. It's a strategy that works particularly well for landowners who want to simplify their estate, divide ownership among heirs, or move toward retirement without triggering a massive tax event.

Section 121: Primary Residence Exclusion

This one technically applies to homeowners, not farmland, but it comes up more often than you'd think in agricultural situations, especially when a home sits on the same parcel as farm ground.

What it does: Section 121 allows homeowners to exclude up to $250,000 ($500,000 if married filing jointly) of capital gain from the sale of their primary residence, provided they've owned and lived in the home for at least two of the last five years.

Why it matters for landowners: If your farmstead includes a home you've lived in, the residential portion of the sale may qualify for the Section 121 exclusion while the agricultural portion can potentially be handled through a 1031 exchange. This combination, sometimes called the "1031/121 Combo," can be incredibly powerful. In some cases, it can reduce a tax bill from hundreds of thousands of dollars to effectively zero.

Important nuance: If you've lived in the property up until the sale, you must sell within three years of moving out to still qualify for the 121 exclusion. For mixed use properties (like a house on a farm), gains are allocated proportionally between the personal residence portion and the investment/business portion.

Section 179: Immediate Expense Deduction for Business Assets

This is one of the most farmer friendly provisions in the tax code, and it gets used every year by operations across the country.

What it does: Section 179 allows businesses, including farming operations, to deduct the full purchase price of qualifying equipment and certain property improvements in the year they are purchased, rather than depreciating them over several years.

Why it matters for farmers and landowners: If you buy a new tractor, grain bin, irrigation system, or certain farm structures, you may be able to write off the entire cost in the current tax year. For operations that have a strong income year and need to manage their tax exposure, Section 179 is often the first tool they reach for.

The annual deduction limit has been quite generous in recent years (over $1 million for qualifying property), though it phases out as total equipment purchases exceed certain thresholds. The specifics change from year to year, so this is one where staying current with your CPA matters.

Section 180: Soil and Fertilizer Expense Deduction

This is a smaller provision, but it's tailor made for landowners who are investing in the long-term health of their ground.

What it does: Section 180 allows farmers to deduct expenses for fertilizer, lime, and other materials used to enrich or condition farmland soil in the year those expenses are incurred, rather than capitalizing them.

Why it matters for landowners: If you're putting money into soil health, whether that's lime applications, fertility programs, or other soil conditioning work, Section 180 allows you to deduct those costs right away.

But here's where this section gets really interesting, and where most landowners and even many CPAs are leaving significant money on the table.

The Overlooked Deduction: Soil Fertility Value at the Time of Purchase

When you buy a piece of farmland, you're not just buying dirt. You're buying decades worth of nutrient buildup that the previous owner invested in. Phosphorus, potassium, lime, and other nutrients that have been applied over years of farming don't just disappear. They remain in the soil profile and have real, measurable economic value.

Companies like Boa Safra specialize in exactly this. They work with landowners and their tax advisors to quantify the fertility value embedded in the soil at the time of land purchase. Through detailed soil sampling, laboratory analysis, and agronomic valuation, they determine how much of the purchase price is attributable to the "excess" soil fertility that exists above a baseline level.

Here's why that matters: when that fertility value is properly documented and separated from the land purchase price, it can potentially be deducted under Section 180 as a soil and fertilizer expense, rather than being lumped into the non-depreciable cost of the land itself. Land, as we know, cannot be depreciated. But the fertility that's in the land? That's a different story.

Think about what this means in practical terms. You buy a farm for $10,000 an acre. A qualified analysis determines that $800 per acre of that value is attributable to excess soil fertility built up by the previous owner, nutrients like phosphorus and potassium that are sitting in the soil and will be consumed by future crop production. That $800 per acre may be eligible for deduction, turning a portion of your land purchase into a current year tax benefit.

On a 160 acre farm, that could translate to over $125,000 in potential deductions that most buyers never even think to claim.

This isn't a new concept, but it's one that the agricultural tax world has only recently started paying serious attention to. For years, the entire purchase price of farmland was simply allocated to "land" on the balance sheet, and the fertility value was ignored. Firms like Boa Safra are changing that by providing the detailed, defensible analysis that supports the deduction.

Important considerations: This strategy requires proper documentation, including professional soil testing, agronomic valuation, and coordination with a CPA who understands agricultural tax. The IRS expects a reasonable and well supported allocation, so this is not something you estimate on a napkin. But when it's done correctly, it's one of the most overlooked deductions in all of farm tax planning.

If you've purchased farmland in recent years and never had a soil fertility valuation done, it's worth a conversation with your tax advisor. You may be sitting on a deduction you didn't know existed.

Section 167: General Depreciation Rules

This is the foundational section that establishes the rules for depreciating tangible property used in a trade or business or held for income production.

What it does: Section 167 lays out the general framework for recovering the cost of business assets over their useful life through annual depreciation deductions.

Why it matters for landowners: While the land itself is not depreciable (it doesn't wear out or get used up), the improvements on it absolutely are. Buildings, grain storage, fencing, drainage tile, and other structures all have depreciable lives. Section 167 is the starting point for understanding how those deductions work, though most farmers will actually apply the more specific rules found in Section 168.

Section 168: MACRS Depreciation System

This is where Section 167 gets put into practice with specific timelines and recovery periods.

What it does: Section 168 provides the Modified Accelerated Cost Recovery System (MACRS), which is the primary depreciation method used in the United States today. It assigns specific recovery periods to different types of property: 5 year property (certain farm equipment), 7 year property (most machinery, office furniture), 15 year property (land improvements, drainage, fencing), 20 year property (farm buildings), and 27.5 year property (residential rental).

Why it matters for farmers and landowners: When you invest in drainage tile, build a machine shed, or install fencing, Section 168 determines how quickly you can write off that cost. The accelerated nature of MACRS means you recover costs faster in the early years, which can significantly reduce your tax burden in the years following a major capital improvement.

Bonus depreciation has also been a major factor in recent years, allowing even faster write-offs on certain qualifying property. However, bonus depreciation percentages have been phasing down, so the specifics depend on when the asset was placed in service. Your CPA can walk you through what applies to your situation in the current tax year.

Section 611: Depletion of Natural Resources

This one applies to a more specific group of landowners, but it can be very valuable for those who qualify.

What it does: Section 611 allows a deduction for the depletion of natural resources, including timber, minerals, oil, and gas. Depletion works similarly to depreciation, but instead of a building wearing out over time, a natural resource is being extracted and reduced.

Why it matters for landowners: If you own timberland and harvest trees, or if you have mineral rights with active extraction, Section 611 allows you to deduct the declining value of that resource base over time. For landowners in areas with active oil, gas, or mineral production, this deduction can be substantial.

There are two methods of calculating depletion (cost depletion and percentage depletion), and the rules differ depending on the type of resource and the taxpayer's involvement. This is another area where working with an experienced tax professional is essential.

The Bigger Picture

Here's what I really want you to take away from all of this.

The tax code is complicated. Nobody is arguing that. But buried inside all that complexity are provisions that were specifically created to help people who own land, farm it, and invest in real property. The landowners who benefit most from these sections aren't the ones with the fanciest accountants. They're the ones who take the time to understand what's available and start the planning conversation before they're in the middle of a transaction.

Whether you're thinking about selling, buying, improving, or simply holding your land, at least a few of these code sections probably apply to your situation right now.

The best next step? Have a conversation with your CPA or tax advisor and ask specifically about the sections that seem relevant to you. Bring this article with you if it helps. The goal isn't to become a tax expert. The goal is to make sure you're not leaving opportunities on the table.

Your land is one of the most valuable assets you'll ever own. The tax code has more tools to help you protect it than most people realize.

A Clear Summary: IRS Code Sections for Landowners

Disclaimer

The information provided in this article is for general informational and educational purposes only and does not constitute legal, financial, or tax advice. Tax laws are complex, subject to change, and vary based on individual circumstances. The IRS code sections discussed here are summarized in plain language for accessibility and may not reflect every nuance, limitation, or qualification that applies to a specific taxpayer's situation.

Readers should consult with their own qualified legal, tax, or financial advisors before making any decisions based on the content of this article. Neither Steve Link, Pifer's Auction & Realty, nor any affiliated parties make any guarantees as to the accuracy, completeness, or applicability of the information presented. Any examples used are hypothetical and for illustrative purposes only.

This article does not constitute an offer to buy or sell securities or real estate. All investing and real estate transactions involve risk, including the potential loss of principal. Past performance of any asset class, investment strategy, or tax outcome is not indicative of future results.

Author Bio: Steve Link is a broker with Pifer's Auction & Realty, specializing in farm, ranch, and recreational land across the Upper Midwest. Steve grew up on a farm near Milan, Minnesota and earned a degree in Natural Resource Management from North Dakota State University. With decades of experience in land sales, auctions, and land management, Steve works closely with landowners, investors, and agricultural operators to help them make informed decisions about one of their most valuable asses: land.